May 1, 2026 - Tax Diversification: The Three-Legged Stool of Personal Savings

Some savers and investors may know about the "original" three-legged stool. It includes Social Security, a Defined-Benefit Plan (a.k.a pension), and personal savings:

This is the traditional three-legged stool when people think about their income during retirement

Retirement planning has changed. The old three-legged stool of Social Security, a pension, and personal savings—isn't as sturdy as it once was, which means today's investors need to build a stronger foundation of their own.

Clients I work with express fears and doubts about the reality of this model. They fear that Social Security will be reduced or their full retirement age will be pushed out when they retire. Defined-benefit plans (pensions) are rare anymore - typically public institutions like schools and governments have them, but many private businesses do not. This leaves only one leg of the stool that people feel is within their control.

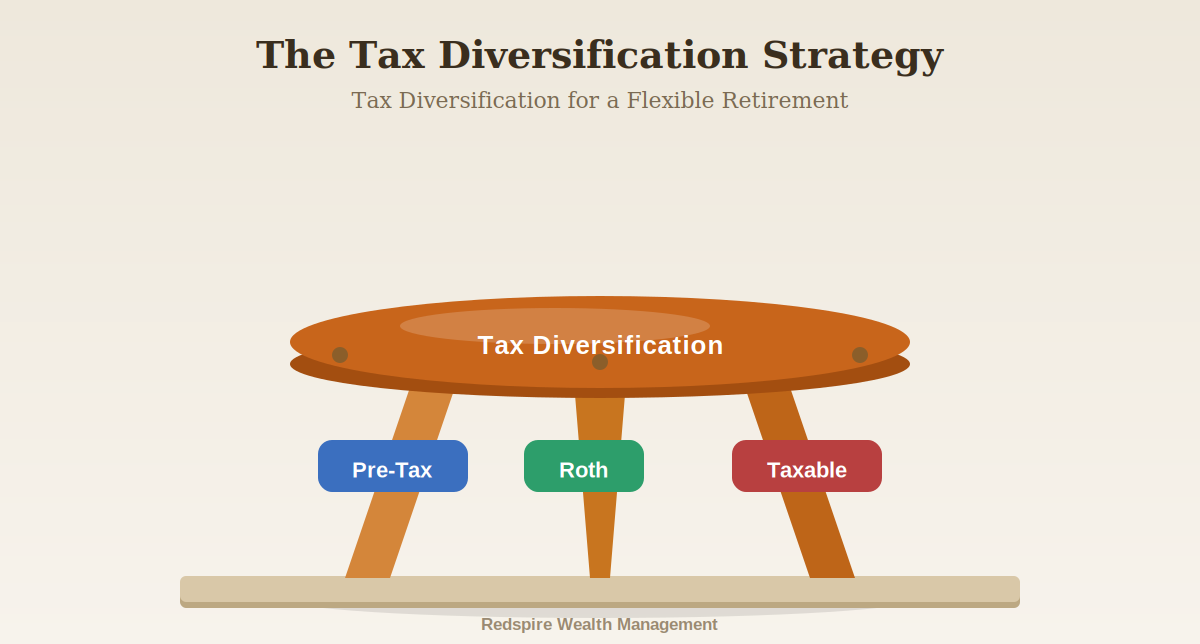

Personal Savings

Personal savings for retirement is often associated with a workplace 401(k). While a workplace 401(k) can be a highly-effective tool for retirement savings, it often becomes the default and only place where people are saving. Unbeknownst to many savers, their 401(k) is likely full of pre-tax funds which could present a problem during retirement. That's why there should be a three-legged stool for personal savings:

Personal savings is largely within our control. Where we allocate those dollars have an impact on retirement.

Leg #1: Pre-Tax Savings

This is the bucket most people are familiar with. We save in a 401(k), lower our taxable income in the year we contribute, and withdraw funds during retirement.

401(k) plans often provide a profit-sharing or matching contribution from the employer which make them excellent accounts for retirement savings. Contribution limits for 401(k)s are high so workers are encouraged to save substantial amounts of their incomes.

This doesn't come without caveats. Funds typically can't be accessed without penalty until age 59.5 with few exceptions. Pre-tax savings, whether in a 401(k) or IRA, will have required minimum distributions (RMDs) starting in your 70s. Since withdrawals are taxable income, there could be a scenario where funds are not needed but withdrawals are required. This can push up taxable income to higher tax brackets.

Leg #2: Roth

Roth IRAs are a common way to save for retirement. 401(k)s can have a Roth option, too.

The idea is simple: Roth contributions are made after-tax so that growth, dividends, interest, and withdrawals are all tax-free during retirement. This can be especially useful when one's income during retirement can impact the taxation of Social Security and the cost of Medicare.

Just like pre-tax 401(k) savings, there are some limitations on Roth IRA contributions. There are earnings limits on Roth IRAs so if you make too much, you cannot fund a Roth IRA directly. Funds can't be accessed without penalty and taxes before age 59.5 with few exceptions (contributions can be withdrawn anytime, but withdrawing earnings early may incur taxes and penalties). The contribution limit for Roth IRAs is relatively low so there's only so much you can contribute over the course of your career.

Leg #3: Taxable

This is probably the most overlooked way to save for retirement. Many young savers and investors treat the taxable money in their Robinhood account as their day-trading account rather than a long-term retirement account. But, when you explain to them that it can facilitate early retirement their attitude shifts.

There are no contribution limits or earnings limits to a taxable account (sometimes called an individual, joint, or brokerage account). The investment options are more flexible in taxable accounts compared to employer-sponsored plans (401(k)s) or Roth IRAs. There is no early withdrawal penalty for taxable accounts - funds can be accessed at any age.

Taxable accounts are not without drawbacks. Interest, dividends, and realized gains are taxable in the year they occur. Qualified dividends and long-term capital gains taxes are lower than the ordinary income rates, so that may help savers get over the fact that taxes are owed even if they don't make withdrawals.

Summary

The stool will not stand without all three legs. This doesn't necessarily mean that every leg is "equal." There are many valid reasons why someone might have more pre-tax assets than taxable assets, for example.

A financial plan will review how much is in pre-tax, Roth, and taxable accounts. That's just the beginning. A financial plan can tell you how much should be in each bucket for the goals you want to achieve (like early retirement) and how to get there.

A well-built retirement plan doesn't rely on a single account or strategy. It balances pre-tax, Roth, and taxable savings to create flexibility, tax efficiency, and confidence before and throughout retiremen